Consider the possibility of a cyber attack on your small business. All data is lost, business cannot be operational, and clients are in danger; this is the reality for many SMEs. Nearly half (46%) of cyber breaches affect businesses with under 1,000 employees. Cyber insurance comes in as a financial instrument that helps to recover losses in the event of a breach.

The most important question is; how effective is this insurance in preventing the loss to one’s business, is it the lifeline your business needs, or just another bill to pay? Let’s dive into the world of digital insurance and find out whether it’s an affordable safeguard or an unnecessary luxury.

What is Cyber Insurance?

Cyber insurance is a countermeasure that enables businesses to offset costs due to damages caused by a cyber attack. Small companies cannot deal with cyber issues like data losses or ransomware attacks. On average, small and medium-sized businesses (SMBs) face cybersecurity costs ranging from $826 to $653,587 per incident.

Cyber risk insurance assists in incursions of this nature helping businesses bear the burden; It employs the same principle as other cyber insurance covers, businesses are charged certain premiums according to the coverage offered and in case of an attack, money is reimbursed to these companies.

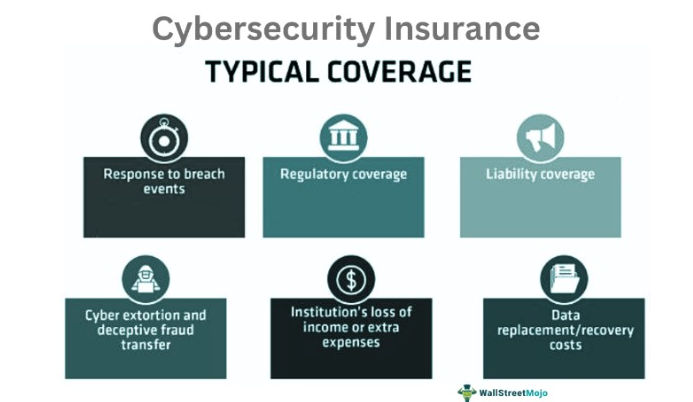

Protection by cyber liability insurance is usually focused on responding to data breaches by providing assistance and notifying affected customers, It also includes coverage for possible litigation expenses due to breach lawsuits.

Expenses that arise due to various physical losses of income due to cybercrime can also be covered under the insurance policy. Some policies pay for the cost of ransom, minimizing emergency risks.

Particularly when dealing with common cyberattacks, digital insurance is very important. Suppose a small company is a victim of a ransomware attack, cyber insurance policy will pay the ransom, cover the repair of the IT systems, and legal advice. If there is a breach of security, this policy helps defray the cost of informing clients, recovering data, and expenses related to litigation. In a situation where an employee’s confidential information has been exposed due to phishing fraud, cyber insurance also handles such financial risks.

The Growing Cyber Threat Landscape for SMEs

Lately, cybercriminals have begun to focus on small and medium-sized enterprises (SMEs). 43% of cyber-attacks are targeted at SMEs, and nearly 60% of the SMEs go out of operation within 6 months of a major cyber incident. This indicates a strong need for SMEs to understand the improved trend in the environment concerning cyber threats.

Small and medium enterprises lack robust security integration as it is mostly seen among large organizations. Some have outdated platforms while others dedicate a limited budget for cyber security. Furthermore, with the new normal of working from home, there is potential for employees to create security problems by using insecure connections or equipment. Enhanced phishing and malware attacks have increased vulnerability for SMEs which exposes them to even more risk.

There have been some incidents in cyberspace that have evidenced the severity of such threats. In 2021, a cyberattack that involved ransomware on a big software company affected many small and mid-sized enterprises across different sectors crippling their operations and exposing data that should be classified.

Another incident of note was that of a small healthcare service whereby customer’s data was breached leading to the imposition of penalties and loss of patients’ confidence. Such issues not only lead to massive monetary loss but also reputation that took years to build.

The Benefits of Digital Insurance for SMEs

Small and medium enterprises suffer the most in terms of financial losses due to cyberattacks. A single data loss because of hackers can cost thousands if not millions in recovery, regulatory fines, and even loss of revenue. Cyber insurance answers one pivotal aspect by offering nominal financial resources to cater for the expenses incurred in the response to such attacks and reducing the losses to be incurred by the business.

The occurrence of these attacks leads to complexities from a legal perspective. These costs include regulatory, notification, and litigation-related costs which digital insurance mitigates. Further, many policies include incident response assistance to facilitate the recovery process enabling business operations to continue as quickly as possible without bearing the full financial burden.

A data breach can have a very major effect on a firm’s image and the trust of its clients. Only around 14% of small businesses believe they are sufficiently equipped to protect themselves from cyber threats. Cyber insurance not only helps mitigate immediate financial losses but also aids in long-term reputation management. By demonstrating a commitment to cybersecurity, businesses can reassure customers that they are taking steps to protect their information, ultimately strengthening their brand.

Insurance companies that provide coverage against cyber risks often have great capability and resources in the provision of cyber risk management services. SMEs can be advised on how to best protect their data and minimize the risks they are facing. Insurers may provide cyber security software solutions, training, and systems assessment to enable businesses to prevent future incidents.

Is Cyber Insurance Affordable for SMEs?

The emergence of cyber hazards for small and medium enterprises (SMEs) raises a question on the affordability of cyber insurance. Approximately 13% of small and medium enterprises (SMEs) currently have cyber insurance. This low adoption rate indicates that numerous SMEs may consider the expense too high or lack awareness of the advantages it offers.

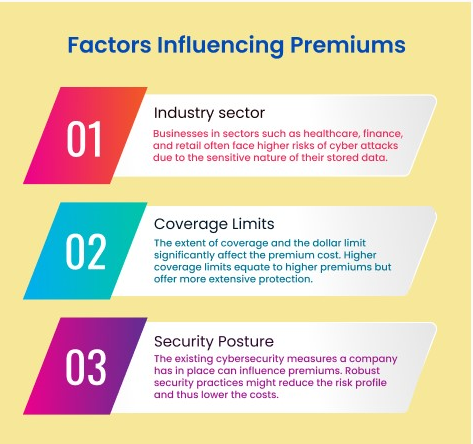

To shield your businesses with appropriate digital insurance, it is helpful for SMEs to understand the costing attributes when it comes to premiums billing. There is a great variation in the amount of digital insurance premiums charged or offered. Generally, when underwriting policies, insurers take into account the company size, the nature of the business, and the extent of the implemented cybersecurity measures.

For example, a firm that has good security measures may pay lower rates compared to one that does not. In addition, the extent of cyber insurance coverage needed, be it for data breaches or ransom theft, will have a considerable impact on the rates charged. Particular risk profiles must be determined by businesses to quantify the extent of coverage they need.

In terms of premiums, SMEs on average pay less than bigger businesses because of the size and the risk profile as well. However, this is not to say that for SMEs insurance is always within reach. Big businesses on the other hand have the advantage of applying and having powerful cybersecurity policies and practices hence when they insure, they get better limits. There is a potential risk where SMEs have to tread carefully to strike a fair price to protect their businesses adequately.

One of the advantages of digital insurance is the ability to tailor policies to meet specific needs and budgets. SMEs can adjust deductibles and cyber insurance coverage limits to align with their financial capabilities. For instance, opting for a higher deductible may lower premium costs but requires careful consideration of potential personal expenses in the event of a claim. Additionally, businesses should explore bundling insurance products or seeking group rates through industry associations to secure more competitive pricing.

Potential Downsides of Digital Insurance

The importance of cyber risk insurance cannot be stressed enough, however, it has some shortcomings. For SMEs, these criticisms are important to consider before a purchase. Here’s what you need to know:

1. The Limits of Cyber Insurance: What It Doesn’t Cover

Even though a cyber insurance plan seeks to secure a business from several attacks, there are gaps in coverage. For example, the scope of coverage is often limited to operational downtime and does not extend to pre-existing weaknesses and internal misconduct. Additionally, some plans won’t cover fines or penalties from regulatory bodies, leaving businesses exposed to unexpected costs.

2. Potentially High Deductibles and Complex Claim Processes

Upon reviewing policies, it becomes apparent that many digital insurance policies carry what is known as a retention amount or deductible. Some organizations have complex claims processes that may require evidence of loss by making a proof of causation which may take time.

3. The Misconception That Insurance Replaces Cybersecurity Measures

One of the pronounced errors is thinking that because a business has digital insurance, there are no requirements to put security measures in place. It is not uncommon for insurers to require that such companies comply with stringent security policies and enforcement. Such exclusion measures could lead to businesses experiencing more claim denials or an increase in policy premiums.

Cyber Risk Insurance vs. Strong Cybersecurity Practices

As more cyber threats arise, small and medium enterprises (SMEs) are presented with a critical dilemma, is cyber insurance sufficient, or should there be further investments into better cyber security practices?

Insurance offers security and coverage in the event of an attack. However, it should never take the place of protective measures. Policies may offer protection from other expenses such as legal actions, data recovery, and paying of penalties but it cannot stop the attacks from occurring, it is merely a compensatory service and does not prevent incidents. Cybersecurity tools like firewalls, encryption, and system monitoring, protect and mitigate the threats against a business.

Policyholders should be extremely careful regarding relying only on insurance policies. Cyber risk insurance policy may not suffice for the coverage of all kinds of cyber terrorism and where there are poor defenses, the losses could exceed what the insurance can reimburse. In addition, several incidents can take a toll on the company’s brand which may mean losing clients, something insurance money can’t always fix. Prevention through solid security practices is always better than reaction.

When insurers evaluate a business for cyber insurance, they look closely at its cybersecurity measures. Businesses with weak security practices often face higher premiums or even struggle to get coverage. Insurers reward companies with strong defenses, such as multi-factor authentication and employee training, because they pose a lower risk.

Do SMEs Really Need Cyber Insurance?

As cyber crimes are more prevalent within modern society, it has left many small and medium enterprises wondering whether there is a need for cyber insurance or whether it is just another expense. Evaluating answers to the query depends on various criteria including, the size of the business, the type of industry, and risk profile. 62% of SMEs with developing cybersecurity practices consider cyber insurance valuable for the protection it provides.

For a few SMEs, especially those privy to sensitive information of customers or those in financial and health services, cyber insurance coverage against cyber risks is necessary. These companies operate at higher business levels; for instance, a data breach would end up attracting huge costs and legal suits. In contrast, smaller companies with minimal online presence may see that the risk exposure does not warrant the policy costs.

There are other ways in which SMEs would be able to address the issue of cyber risk; for example, businesses that do not have broad risks of cyber exposure may be a self-insuring filing or setting aside funds to cater for projected attacks. In addition, investing in enhanced IT security measures, such as firewalls, encryption, and employee training, can significantly reduce vulnerabilities, potentially making digital insurance less critical.

Specific situations exist in which the purchase of cyber insurance holds meaning. Companies performing a high volume of transactions or retaining critical information of clients should consider this insurance to avoid incurring expensive losses. However, Low-risk SMEs with well-developed cybersecurity infrastructure are likely to regard tech insurance as an unnecessary cost instead of a need.

How to Choose the Right Digital Insurance Policy

Selecting the right cyber insurance policy is essential for small and medium enterprises (SMEs) looking to safeguard against the growing threat of cyberattacks. With various options available, understanding key factors can help SMEs make informed decisions.

Key Factors to Consider

- Coverage Options: Look for a policy that offers comprehensive cyber insurance coverage tailored to your business’s specific needs. This should include protection against data breaches, ransomware attacks, and other cyber incidents relevant to your industry.

- Premiums: Check whether the quote given on the policy warrants the risk burden. It is imperative to analyze the range of rates to ascertain whether the outlined benefits are worth the mentioned costs. Most importantly, cheaper premiums may mean less coverage; hence moderation must always be sought.

- Claims Process: The claims process must not be cumbersome. Check how claims are made with your current insurer, and how the customers feel about their claims department. Most Claims processes tend to determine the extent of recovery in times of a disaster.

To select appropriate coverage, assess your business’s risk profile. Consider factors like the size of your company, the sensitivity of the data you handle, and your existing cybersecurity measures. This evaluation will help determine the level of coverage necessary to protect against potential losses.

Make sure you always go through the policy to avoid any surprises when filing a claim. Focus on exclusions, deductibles, and coverage limits. With this clarity, you will be able to know what is covered and what is not covered in the policy enabling you to make a wise choice.

Weighing Value Against Cost

Cyber insurance for SMEs becomes a question of weighing the amount of protection from this potential investment against the capital that would be paid out for the insurance policy. By evaluating your specific business threats and the consequences of a cyber breach, you can decide whether this cover is worth investing in or is an unnecessary cost.

The post Cyber Insurance for SMEs: Affordable Protection or Unnecessary Expense? appeared first on Datafloq.